Introduction

The reliability of p2p loans lies in the credibility of the p2p lending platform you are using. It is the duty of the p2p platform to ensure that only borrowers with good credit score and or credit history are accepted while rejecting those that do not meet the minimum borrowing requirements. This way, lenders will be guaranteed to receive their invested capital plus interest.

If you are planning on investing in p2p loans and don’t know how to find reliable loans, I am going to share with you some tips on how to go about it.

As mentioned above, loan reliability depends on the platform you chose to use, so essentially, this means platform reliability equals loan reliability.

Since lenders are allowed to select who they want to loan their money, the approval process with peer to peer loans may be a bit flexible compared to traditional lenders such as banks and credit unions. Some platforms may even use unconventional data to determine the creditworthiness of a borrower. With the advancement in technology, platforms are also using artificial intelligence algorithms and other tools along with credit scores to find reliable borrowers.

How to find trustworthy p2p platforms with reliable loans

The key people

Most people when determining the credibility of peer to peer loans, they ask the following questions:

- Are the listed loans secured?

- Does the platform have a provision fund to pay off bad debts?

- How much has been lent so far?

- Have lenders lost any money?

- How long has the platform been in business?

While those are genuinely relevant and important questions, the first thing you should always find out is if the platform has the right people.

If you look at the current p2p lending platforms, they should all have one thing in common; key people with relevant experience. So before deciding to put your money on any loan, make sure you check the professionals behind the platform. If the platform doesn’t have the right individuals, it may be better to wait until they have a great track record.

When it comes to finding reliable p2p loans, it will serve you best to put staff (co-founders, board members, and other key individuals) above everything else such as bad debts, interest rates, and borrower credit rating.

A little research online on the founders can help you in your quest for finding the reliability of a platform. Though you can’t rely on the information you find online, it is still a great starting point.

So, on the platform’s website, go to “About US” or “Our Team” and look at the profiles of the founders and other staff members. Ideally, if the platform has dedicated this section to list the names of the staff, it is for marketing purposes and chances are good you will find a lot of details on each individual.

Basically, what you want to look for in the staff composition includes:

- Credit assessment profession

The person in charge of credit assessment should have relevant experience in banking. This means that the person had experienced and maybe even devised an effective process needed to take a preliminary assessment of borrowers and their security using suitable searches, criteria, and questions, and make a decision whether to lend and at what rate of interest. This requires years of experience among key professionals in the management team.

- Risk specialists

Most p2p lending platforms today use data scientists instead of old versioned risk specialists. While that is ok, it is still important to have at least one data scientist with loan risk analysis or loan risk modeling experience. A risk specialist should also have a decent compliance experience.

- Credit committee

There should also be a credit committee comprising experienced individuals that decide whether to approve loans or not.

Quality of security

Though most peers to peer loans are unsecured, there are those that are secured. For secured loans, you want to make sure that the attached asset is of good quality. However, a good p2p lending loan should only use security as a last resort. As a result, they will go for quality security but still allow only quality borrowers to their platform.

A platform that relies on security too much may result in too many defaults. This may mean that the people behind the p2p lending company are single-minded and are only focused on overnight growth.

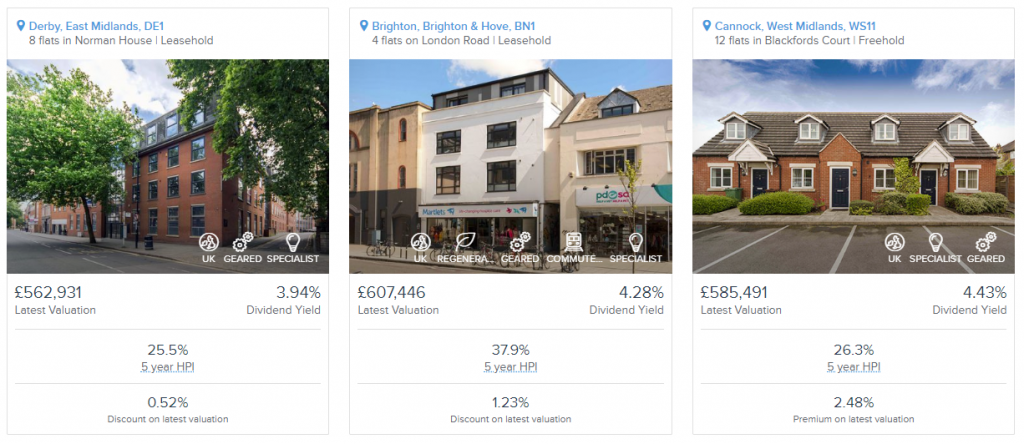

Loan to value (LTV)

Loan to value ratio is an important thing to consider when deciding whether or not to fund a loan. The LTV is the proportion between the loan and the total value of the asset purchased with the loan (imagine for example a house and the loan attached to it). Ideally, a p2p lending should always have a loan to value of at most 80%.

This LTV parameter is mostly common with property loans. You will often see the abbreviation “LTV” next to property loans, but it usually doesn’t mean what you may think. Ideally, what the site should write is “LGDV” – gross development value, which is a hoped-for-sale price of the property after it has been completed and sold.

While this value is not always an indication of reliable loans, there is a better way you can establish the real LTV of a property development loan. Just find the real value of the land and property in the current market and compute the loan amount against that value.

[insert page=’cta-footer-crowdlending’ display=’content’]