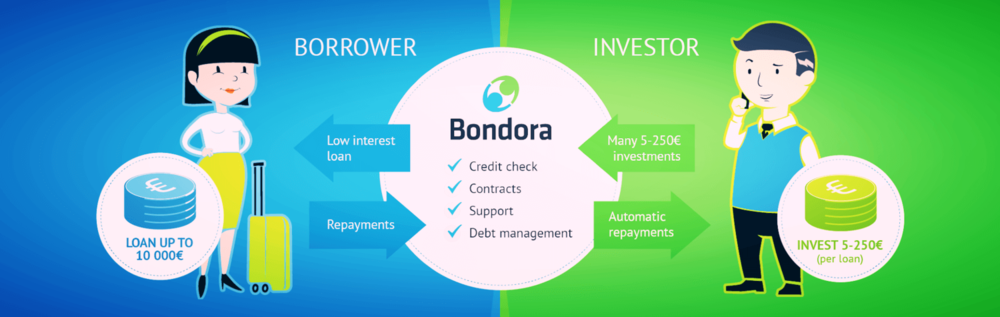

Peer-to-peer lending or p2p lending or Crowdlending enables persons to borrow loans directly from other private individuals, thus cutting out the traditional financial institution as the middleman. The whole operation takes place online, through a platform that matches borrowers with lenders (investors).

In recent times, these platforms have significantly increased their adoption as a viable alternative method of financing.

Peer-to-peer lending has many aliases, including “social lending” or “marketplace lending”. The concept has existed only since 2005, but the competition is already stiff especially in markets such as China, Europe, and North America.

Detailed Understanding of Peer to Peer Lending

So what exactly is peer to peer lending?

Peer to peer platforms link borrowers directly to investors. The interest rates of each loan vary from one platform to another, as well as the terns of transactions. Most p2p lending platforms have a wide range of rates based on the borrower’s creditworthiness.

The process starts with an investor opening his account on the platform and then depositing a certain sum of money that he is planning to invest. The limit amount also depends from one platform to another.

The investor then creates an investment profile where he can usually set the target ROI of investments, the investment term and the country. The investor will then be availed with a variety of loan offers, from which he can review and invest in.

The process of money transfer and the monthly interest’s repayments are taken care of by the platform. The entire process is generally automated.

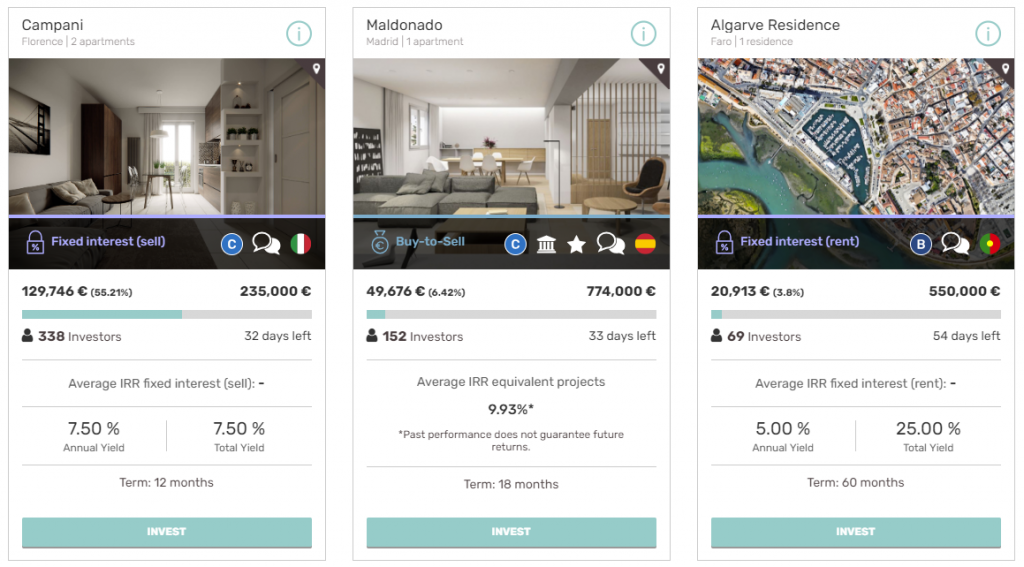

Different sites specialize in different types of loans or types of borrowers. For instance, Crowdestor and Grupeer are designed for real estate and business projects while Mintos is mostly focusing on consumer lending.

The Evolution of P2P Lending

Since the first p2p lending platform was launched, peer to peer lending has undergone some tremendous changes. In its early stages, peer to peer lending was only seen as an option for providing credit access to individuals who would be rejected by traditional institutions or a mean to consolidate a student loan debt at affordable rates compared to traditional banks and credit unions.

However, recent years have seen a shift in the landscape for p2p lending as most platforms have expanded their reach. For instance, most sites are now targeting consumers who are looking to pay off their credit card debt at affordable or much lower interest rates. There are also a lot of other options such as home improvement loans and auto financing.

Borrower with good credit ratings will enjoy much lower interest rates, sometimes lower than comparable bank interest rates, while applicants with a sketchy credit history will have to pay high-interest rates.

For investors or lenders, p2p lending is a great way to generate interest’s income on their cash at a much higher rate compared to those offered by traditional savings accounts.

Considerations

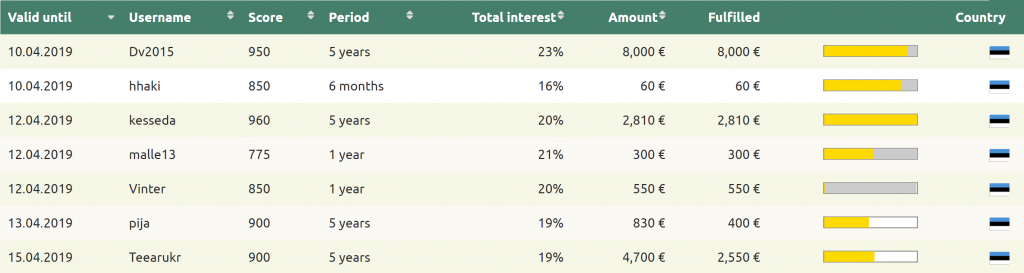

If you are considering joining a peer to peer lending platform as an investor, you need to worry about the default rate. These rates indicate the percentage of loans of an investment platform that are not payed back by borrowers and that will generate a loss of the invested amount. You usually can find this information on the platform you choose, but not all of them provide these sensitive numbers, especially when the platform is still young. For example, Zopa, the first-ever p2p lending site had a default rate of 4.52% for loans offered in 2017 as per the Financial Times, with other platforms forecasting similar default rates.

In comparison, an S&P/Experian composite index of rates of defaults in the United States has been fluctuating in recent years with an average default rate of 0.8% from 2015 to 2019. On the other hand, the default rate on the credit card debt in the United States fluctuated up to 9.1% in 2015 before dropping to 3.56% in 2018 according to Market Watch.

Any borrower or investor considering using Crowdlending platforms should check the transaction fees as well. Every platform has a different business model, but fees and commissions may be charged to borrower, lender, both or neither. Some platforms may charge origination fees, just like the banks, as well as late fees and bounced payment fees. Usually platforms tens to charge the fees to the borrowers.

Some p2p lending platforms may put some restrictions on what types of lenders can invest in the loans. For instance, Lending Club allows anyone to join provided they meet the account minimums. While other platforms may only allow accredited investors and or qualified purchasers. An accredited investor is someone who has a personal income of $200,000 or $300,000 for joint, for the previous two years, or a net worth of more than $1 million, either jointly or individually. On the other hand, qualified purchasers usually must meet even greater requirements compared to accredited investors.

Last but not least, some platforms only allow institutional investors such as commercial banks, hedge funds, pension or endowment funds, and life insurance firms.